These are difficult times for borrowers. Even with moderate easing in 2026, mortgage rates (now approximately) 6.15% for 30-year loans, most of which are expected to remain highCar loan interest rates have recently been around 6.6%, which is a big challenge when the average price of a new car is high

There’s little for consumers to do in this environment besides wait for rates to improve — or, more proactively, improve their credit scores to qualify for lower interest rates.

The average credit score in the U.S. is now 715, which is generally considered “good.” About 25% of consumers have scores in the 740 to 799, or “very good,” range, which qualifies them for better-than-average interest rates. Meanwhile, “exceptional” credit scores of 800 or higher (21% of consumers) qualify borrowers for the best loan terms and rates, according to credit bureau Experian EXPN+2.85% EXPGY+3.66%.

When interest rates come down, “consumers need to be prepared to take advantage of them,” Michele Raneri, vice president and head of U.S. research and consulting at credit-reporting agency TransUnion

It’s amazing+4.34%, told MarketWatch. “If you don’t have a good enough credit score … you’re not going to get it.”

Fortunately, even with a fairly brief window, motivated borrowers can quickly boost their credit scores — some by as much as 100 points — if they make the right moves.

While every person’s credit profile is different, they generally can notice improvements to their score in three to six months, according to FICO

I STAY+0.62%, the credit-scoring company. Some actions could even positively impact a credit report in as little as 30 to 45 days, an Equifax

EFX+3.16% spokesperson told MarketWatch. So if you intend to apply for a loan, plan accordingly.

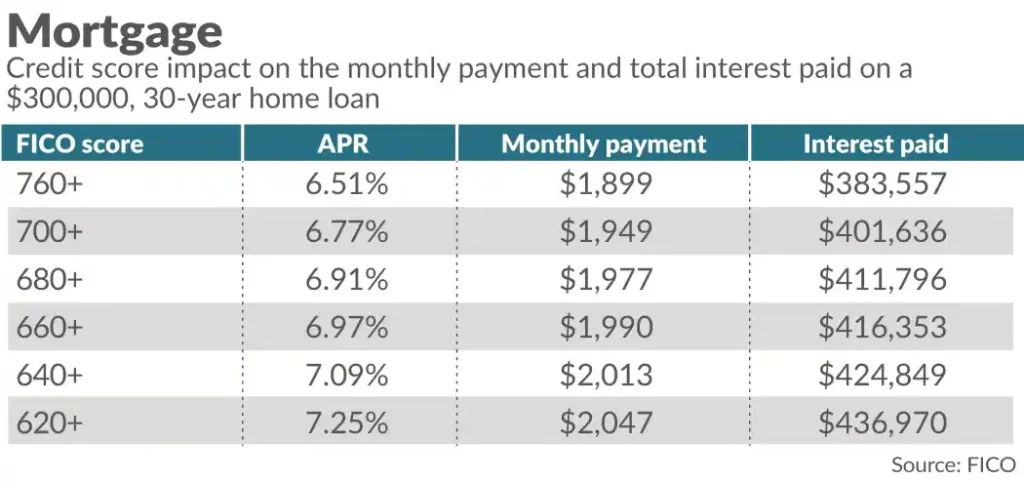

Before we get to some tips, let’s see how impactful credit-score improvements can be on the amount of interest consumers pay. Below are the hypothetical monthly payments on a $300,000 home loan for people with different credit scores — and thus different interest rates — based on FICO’s Loan Savings Calculator. The difference in the total interest paid can add up to tens of thousands of dollars over the life of a 30-year mortgage.

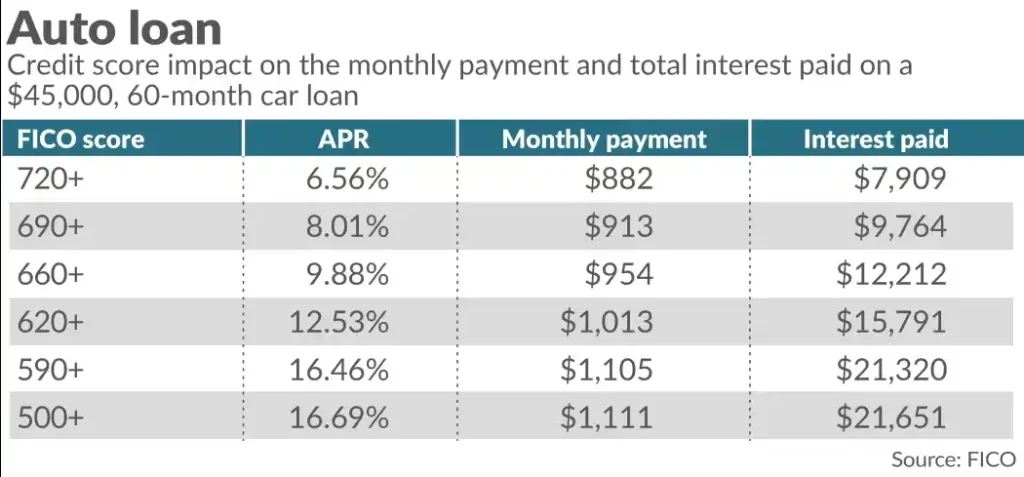

Below is what it looks like for a hypothetical $45,000, 60-month car loan, where interest rates vary more widely than with mortgages. Again, the difference can add up to thousands of dollars over the life of the loan — and for a household that needs to finance a home and a car (or two), interest payments can quickly add up.

Credit experts have developed a process to quickly improve your credit score if you plan to apply for a large loan in 2026. Here are their suggestions:

1. Get up to date on your payments, starting with your most delinquent loan

This is the first and most important step. Your payment history is the biggest part (35%) of your credit score. If you’re reading this story because you’re planning to apply for a big loan soon, be honest with yourself about whether you can afford it if you’ve recently been behind on your other payments.

To meaningfully improve your credit score, start by making a payment on the debt you’re most behind on. “A 30-day late payment is less impactful than a payment that is 60, 90 or 120 days late,” according to Experian.

If a consumer had an unexpected financial shock and can’t afford to pay their balance in full, at least “try to pay the minimum,” an Equifax spokesperson said. This stops the delinquency from progressing and establishes a positive payment history again.

“What you want is to get all of those delinquencies, if possible, in the rearview mirror, as far as you can,” TransUnion’s Raneri said. “Get them as far back as you can, and keep paying perfectly. You don’t have to pay extra, but you can’t have anything be delinquent.” At the three- and six-month marks, your score should be up by several points, she noted.

2. Reduce the amount of credit you are using

The amount of available credit — credit cards as well as other loans, such as a home-equity line of credit (HELOC) — you are using is the second-most important factor (30%) in your credit score. Unlike delinquencies, which take time to get behind you, a change in your utilization rate can be reflected in your credit score in as little as 30 days.

While it is broadly recommended to keep your utilization rate below 30% of your total credit limit, if you’re planning on applying for a loan, maintaining a rate lower than 10% will make your score even better.

Also, remember that maxing out any individual account is particularly unfavorable. People who max out their HELOC may see their credit score take a hit, Raneri said, and the same goes for maxing out a credit card. Having a single card “with a very high utilization rate, such as 100%, can hurt your credit score even if your overall utilization is relatively low,” according to Experian.

How do you lower your utilization rate? If possible, switch to cash, debit or even checks for big monthly expenses like travel, shopping, dining out, groceries and even insurance (which are among the biggest credit-card spending categories) so that you’re not constantly adding to your balance before applying for a loan. To discourage unnecessary impulse spending, remove your credit card from any online stores it is saved on, such as Amazon AMZN+2.90%.

Next, make multiple payments each month — for example, whenever you get paid — to keep the balance from getting too high.

And if you already have more than one credit card, spread out your spending between the cards to stay well below the limit on any individual account. Turn on auto-pay to make them easier to manage.

3. Lengthen your credit history

Length of credit history is 15% of your FICO score. A quick way to lengthen your credit history is to have a trusted person — who, critically, has fantastic credit — add you as an authorized user on their oldest, most spotless credit card. Note: You won’t actually use the card in question — but its payment history and age then become part of your profile, which can boost your score in as quickly as a month or two.

“The biggest jump happens with a thin file that you add that to, because there are so many fewer data points,” said Matt Schulz, chief consumer-finance analyst at LendingTree

Tree+5.73%, whose wife did this to boost their 18-year-old son’s credit score.

This move comes with a warning, however. It is important that the credit card continues to be managed responsibly, which includes not adding charges and jacking up the utilization rate on the account. In a LendingTree analysis of near-prime borrowers (with credit scores of 620 to 659), those whose credit-utilization rates decreased saw their scores rise an average of 3 points three months after becoming an authorized user, while those whose utilization rates increased “saw their credit score plunge an average of 34 points.”

4. Don’t open any new credit cards or close any old cards

This is partly about new credit (10% of the score), and partly about your credit utilization (30%) and length of credit history (15%).

“In the months leading up to a major loan application, try to avoid unnecessary new credit applications. While their impact is smaller compared to other factors, each new application can result in a hard inquiry, and opening new accounts can temporarily lower your scores,” said Experian’s Roman. A hard credit check can take up to 5 points off your credit score.

Meanwhile, if you have an old credit card you aren’t getting much value from anymore, consider waiting until after you apply for the loan to cancel it. “Closing a credit card can negatively affect their credit score by reducing total available credit, which may increase credit utilization and lower the age of their credit file,” Andrada Pacheco, executive vice president and chief data scientist at VantageScore, told MarketWatch.

In terms of length of credit history, the account still stays on your report and will be factored into your score for 10 years, but keeping it open can be handy down the line, particularly if all your other accounts are new. If you’re paying fees for this card, call the issuer and ask if they will waive the fee as a retention offer.

5. Check for errors on your credit report. If you fix any, ask for a ‘rapid rescore.’

One in 20 consumers had errors in their report that affected their credit score or their likelihood of receiving credit, per a Federal Trade Commission study.

Perhaps an error you spotted in your credit report was bringing down your score and just got removed. Or maybe you’ve been doing everything on this list for months, working consistently on improving your credit score, and now you got a pay raise, bonus or some other windfall to pay off a large balance that could put you in a better credit tier.

If you think your credit score has improved since it was last updated, you can ask your home or auto lender for a “rapid rescore,” which quickly adds new payment information to your credit report and updates your score in days (the lender pays for the rescore). Even “a few extra credit-score points gained from recent payments could make the difference in loan approval or save thousands of dollars over the life of the loan,” according to Experian.

Leave a Reply